5. Tax havens help BlackRock push countries into the debt trap

- Antoine Kopij

- 23 hours ago

- 4 min read

Updated: 4 hours ago

In 2021, the Change Finance coalition came together in and around Brussels in opposition to the contract assigned to BlackRock by the European Commission for advising on how to make finance more sustainable.

To help Change Finance, I tried to show that BlackRock not only finances deforestation, but it does so by helping companies and investors elude taxes, thereby denying precious income to developing economies (Blackrock, deforestation and tax havens). I identified tax havens domiciles in a dataset of forest-risk investments managed by BlackRock. Forest-risk investment data was available at the time, but the same research could be done on all investments in lucrative natural resources, because all of them are susceptible to incite capital flight and tax haven financing. Here are some links to academic and NGO investigations in the financing of the extraction of fossil fuels, diamonds and rare metals.

While I was looking at BlackRock’s forest-risk investments, it became clear that all of the countries where BlackRock collects dividends from the slashing and burning of the primary forest are also characterized by high capital flight, indicating plausible profit shifting by the companies involved.

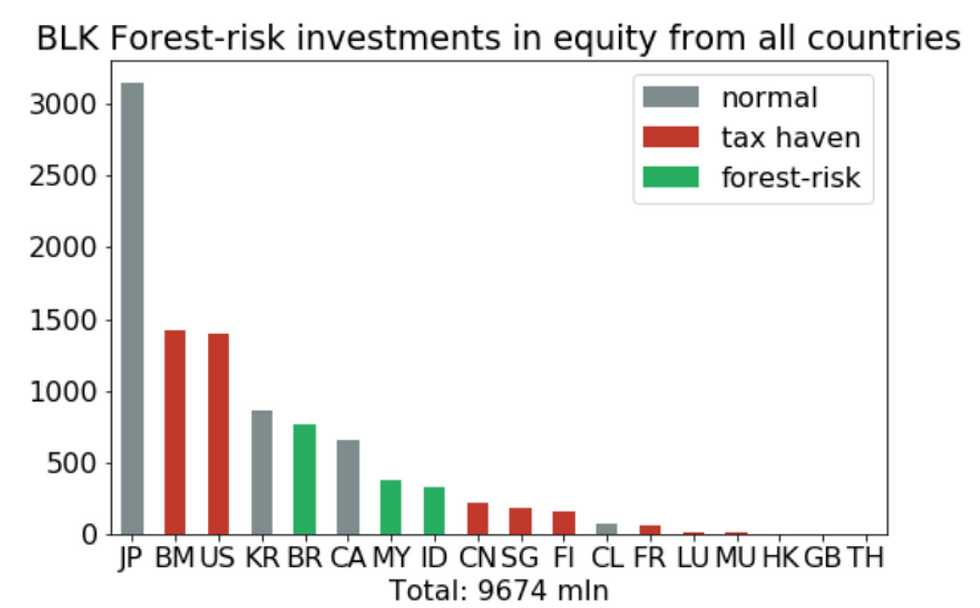

A third of BlackRock's forest-risk investments as of 2021 was routed through tax havens, while only one sixth was destined to companies located in the forest-risk countries themselves. The remaining was invested through companies located in Global North countries. See the barchart below.

The largest single portion (one third) of BlackRock forest-risk investment was destined to Japan (JP), for banking conglomerates investing in coal infrastructure in Vietnam and exploitative plantations linked to forest fires in Malaysia and Indonesia. Although Japan is not considered a tax haven and the country is supposed to be an example on forest conservation when it comes to its national territory, Japanese mega-banks have been denounced as financing Indonesian groups responsible for corruption, land-grabbing and environmental crimes.

Bermuda (BM) and the United States (US), the two largest corporate tax havens in the barchart, together issued the second third of all of BlackRock's equity investment, while the last third was issued by the remaining countries. Brazil (BR), Malaysia (MY), Indonesia (ID) and Thailand (TH) are the four forest-risk countries where forest-risk groups were located and invested in through BlackRock. Together, forest-risk countries issued one sixth of the total. As can be seen in section 2.6 of my report, the four of them are in the top ten countries by capital flight, according to Global Financial Integrity. Since capital flight is considered an indication of tax haven financing, which in turn accentuates the negative effect of the abundance of natural resources in a developing country, it can be assumed that less tax haven financing in forest-risk countries would have a multiplying positive effect on their economies and ecologies. The first plausible effect would be to reroute foreign direct investment from tax havens to the country of operation, thus increasing the small share they have in the current state of BlackRock investments. The ensuing plausible effects would be a decrease in capital flight, improved institutional quality thanks to fiscal revenue, and more income for entrepreneurs thanks to improved infrastructures. Ultimately, according to the model proposed in the Norwegian report on tax havens and development, it would lead to a decrease in rent-seeking and an increase in value creation, while the institutions of forest-risk countries would be better equipped to preserve the rule of law and fight environmental crime.

In the end, the Change Finance campaign was a half-victory. We succeeded in demonstrating that BlackRock shouldn’t be asked to advise on regulating the financial sector, for obvious reasons of conflict of interest. But the European Commission didn’t cancel the contract. It looks as if the Commission is ok with BlackRock being a capitalist monopoly as long as it keeps serving dividends to investors in the Global North.

Launched in 2022, the Debt for Climate campaign has a different goal. This time, a coalition of labor unions, environmentalist and indigenous organizations based in the Global South is claiming the cancellation of their countries’ debt to preserve the climate and the planet’s natural resources. In this perspective, the primary targets of Debt For Climate are the International Monetary Fund and the World Bank, the twin institutions that serve as an interface between debtor countries and their creditors. However, in the antechamber of the negotiations lurks BlackRock, first among investors in fossil fuels and first among private creditors of developing economies.

BlackRock, exemplifying the private financial sector as a whole, obstructs the goals of the Debt for Climate campaign in two distinct ways.

Firstly, as the largest private creditor of developing countries, it repeatedly opposed multilateral debt cancellation and rescheduling organized by the International Monetary Fund, like in the case of Zambia, a country counting on copper mines to pay its debt.

Secondly, as the largest investor in fossil fuels and more generally as the largest (or close second behind Vanguard) investor in the world, BlackRock’s fiduciary duty to its customers dictates that it continues to priorities shareholder value over anything else, thus continuing to expand oil drillings and extracting as much profit from fossil fuels and natural resources as it legally can.

Tax haven financing serves BlackRocks as a tool to maximize shareholder value out of natural resources, but it is also useful in its obstruction to debt cancellation. The presence of vulture funds in secretive tax havens, ready to prey on distressed sovereign debt, is a strong incentive for countries at risk of default to accept harsher conditions for debt rescheduling with the IMF, and higher interest rates for BlackRock. Maintaining their legal domicile in tax havens not only preserves vulture funds from the tax collector, but it also allows them to hide the identity of their traders and investors, thereby avoiding scrutiny from the press and and civil society while allowing institutional investor with a public facing business to participate in their business without facing accountability.

This article is the fifth in a series: Sink logic: how BlackRock and tax havens worsen the climate and debt crisis

Comments